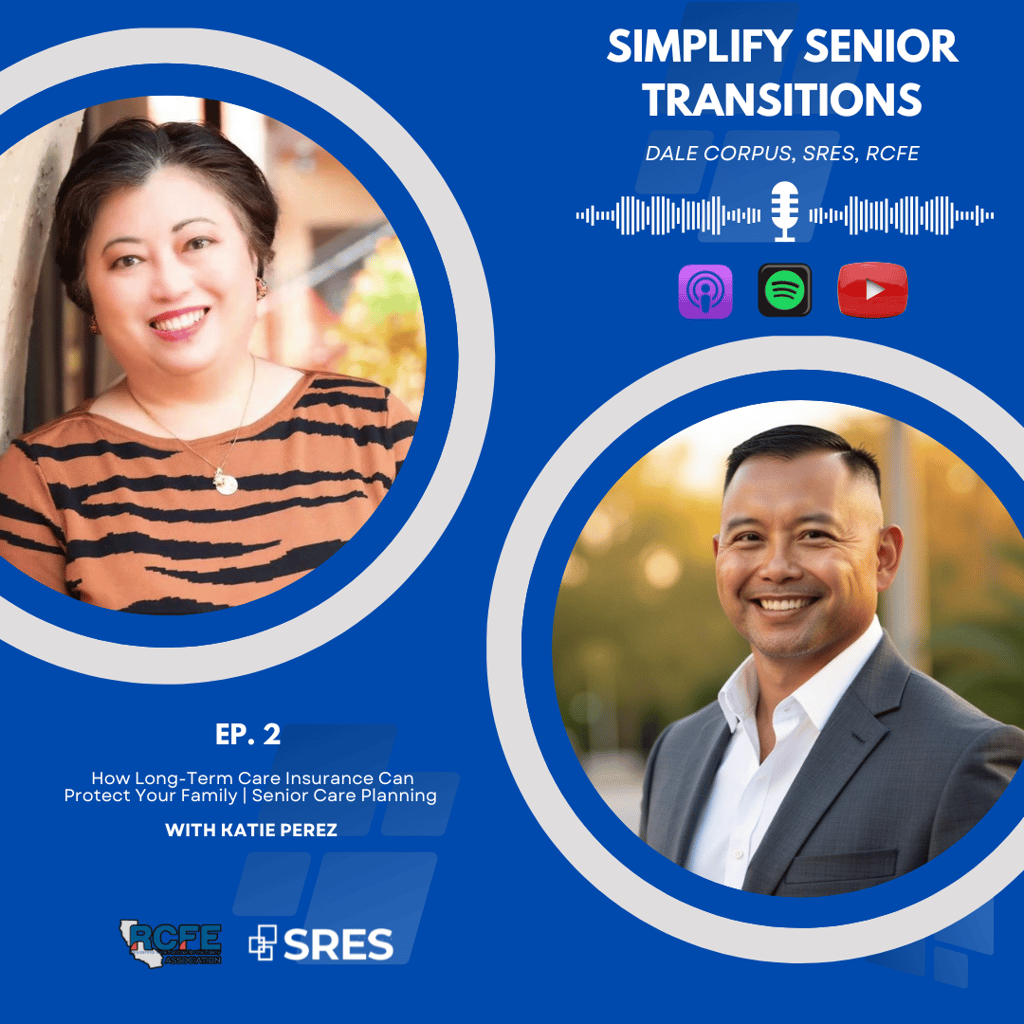

Long-Term Care Insurance in the Bay Area: What Every Family Needs to Know

Dale Corpus

3/5/20254 min read

Navigating the transition for an aging parent can feel like steering a ship through a storm, especially when it comes to the unpredictable currents of senior care costs. If you’re an adult child in the San Francisco Bay Area – from Contra Costa to Napa counties – you know the unique pressures of balancing your own life with the needs of your loved ones. We often hear from overwhelmed family caregivers who are wrestling with everything from downsizing homes to managing emotional stress. That’s why we hosted a crucial conversation on the "Simplify Senior Transitions Podcast" with Dale Corpus, a senior transition specialist and real estate expert, and his special guest, Katie Perez, a long-term care insurance specialist.

Katie's insights are particularly powerful because her understanding of long-term care insurance (LTCI) is deeply personal. Back in 2002, her husband had a stroke at just 54 years old, an unexpected event that completely changed their lives. This firsthand experience of advocating for a loved one made her realize the profound importance of planning ahead for senior care.

Here's what you'll learn in this episode:

Why long-term care insurance matters and how it works.

Who should get long-term care insurance and when's the best time to buy.

Common myths and mistakes people make when planning for senior care.

How long-term care insurance ties into senior transitions and real estate.

Understanding Long-Term Care Insurance: Your Financial Lifeline

So, what exactly is long-term care insurance? By definition, it's for an individual who is diagnosed by a licensed physician as being unable to perform two out of six "activities of daily living" (ADLs) for more than 90 days. These ADLs are basic tasks we often take for granted, like eating, bathing, dressing, toileting, maintaining continence, and moving from a bed to a chair.

It's a common misconception that you'll never need long-term care because you're healthy, or that health insurance or Medicare will cover it. This is not the case; Medicare explicitly does not cover long-term care. LTCI helps you cover a wide range of needs, including home care, assisted living, and nursing homes. It can even cover respite assistance, giving a much-needed break to family caregivers, often the patient's spouse.

One of the most powerful aspects of LTCI is how it helps families afford care without wiping out their life savings. When you self-fund, you might have to tap into your retirement principal, which could jeopardize your ability to generate income, especially if the market is down when care is needed. LTCI protects your carefully built retirement portfolio, ensuring your principal isn't depleted.

Who Needs It and When to Act?

You might think long-term care is only for the elderly, but that's another big misconception. There's no specific age requirement to qualify for long-term care itself. Katie shared a poignant example of a healthy college student who became paralyzed after a freak gym accident in his early 20s, making him eligible for long-term care. In fact, the minimum age to qualify for LTCI coverage is 18 years old.

The truth is, life throws curveballs, and we don't know what the future holds. This is why planning ahead is crucial. The younger and healthier you are when you secure LTCI, the more affordable the premiums will be, and you'll have a better chance of getting covered.

Avoiding Common Mistakes and Navigating Options

The biggest mistake families make is waiting until a crisis hits. When an unexpected health event occurs, your family needs to focus on your care and emotional well-being, not scrambling to figure out financial logistics. Without a plan, someone will inevitably step up, but it often means disrupting their own lives, slowing down their own growth, or putting their family's needs on hold.

Katie describes the superpower of long-term care insurance as the ability to give people time. It removes the immediate pressure to sell assets like your home or stocks, especially if the market is down, allowing your family to adjust to new circumstances, find their rhythm, and then strategically plan for any needs beyond the policy's coverage. This is especially vital in areas like the San Francisco Bay Area, where real estate values, though high, can still fluctuate.

While Medicaid (or Medi-Cal in California) exists as a state and federally funded program, it has strict income and asset restrictions. For many families in the Bay Area who own homes, their assets might exceed these limits, making them ineligible. LTCI, on the other hand, allows individuals to take control of their future and avoid relying solely on state assistance.

If you or your parent are already in poor health, there are still options! While qualifying for traditional LTCI might be challenging, annuity products offering "activities of daily living benefits" with similar eligibility requirements can be explored.

When considering options, don't just look at the cost; understand the value. Make sure you're comparing "apples to apples" by looking at:

Elimination Period: The common waiting period is 90 days, but you can customize it (e.g., 60 days) which affects premiums.

Benefit Period: How many years do you want coverage for (e.g., 5, 7, or 10 years)? This also impacts premiums.

Taxability and Qualified Funds: Understand the financial implications of how benefits are received and how you can fund the premiums.

For every adult child planning for their parents' care, Katie offers this essential advice: Be realistic with what you're willing to give up in your life. While love will make family step up, having professional caregivers through LTCI ensures your family can focus on giving you love and attention without disrupting their own live

Need Help Navigating a Senior Transition?

When a parent needs care and there’s a home involved, families often have more options than they realize. You don’t have to figure it out alone.

Care Funding Calculator

Estimate how income, assets, and home equity may help pay for senior care:

https://www.simplifyseniortransitions.com/care-funding-calculator

Podcast Episode Library

Browse conversations with senior living experts, elder law attorneys, home care leaders, financial professionals, and families navigating these decisions every day:

https://www.simplifyseniortransitions.com/podcastlibrary

Start Here - Personalized Guidance + Resources

Explore resources, ask questions using the AI Resource Explorer, or connect with Dale directly:

https://www.simplifyseniortransitions.com/starthere

P.S. Got news or an amazing story to share? Hit us up at dale@simplifyseniortransitions.com and you might be featured in our next episode! Remember, always check out the transcript for detailed insights. Happy listening!

Watch The Podcast Here

📞 GET IN TOUCH

📬 STAY INFORMED

Dale Corpus, SRES, RCFE

CA DRE# 01305153 | NMLS# 339169

📱 925-380-1657

© 2026. All rights reserved.

🔎 LEARN MORE

PROUD MEMBER OF